Member Tools

These tools and more are available in Web Member Services, the PSRS/PEERS online, self-service membership information portal. Click the links below if you already have a Web Member Services account or register to activate your account.

Tools for Active Members

- View Member Statements

- Estimate Service Retirement Benefits

- Calculate a Purchase Cost

- File for Service Retirement Online

- Designate or Update Beneficiaries

Tools for Retirees and Beneficiaries

Retirement Education

We want to help you learn more about your benefits and retirement system. Our counselors are here to help you get all the information you need, and offer a variety of educational opportunities to best fit your busy life.

Meet the Team » View PSRS Education Options » View PEERS Education Options »PSRS/PEERS News

Big Public Pension Funds' Hedge Fund Portfolios Outperform Their Indexes

Bucking persistent criticism of hedge fund returns coming from many quarters this year, chief investment officers of big state pension funds were able to report strong returns for their hedge fund portfolios.

Sources say public pension plan hedge fund portfolios by design did not keep pace with the returns of the S&P 500 and MSCI All-Country World indexes, which returned 19.7% and 12%, respectively, for the year ended Sept. 30.

That compares to the median one-year return of 9.1% of the 16 hedge fund portfolios in Pensions & Investments' universe as of Sept. 30.

The median of the big public funds topped the 6.4% return of the industry's most commonly used index - the HFRI (Hedge) Fund Weighted Composite, as well as MSCI InvestorForce's Trust Funds' median hedge fund returns for public and corporate defined benefit plans (7.1% and 7%, respectively) and endowments and foundations (6.7%).

"The broad universe of hedge funds tends to be long higher volatility and short lower volatility. We find that a broader mix of strategies is very helpful in smoothing out returns over time," said John Tuck, director of private equity and alternatives for the $37.5 billion Public School and Education Employees Retirement Systems of Missouri, Jefferson City.

That pension fund's $5.1 billion hedge fund portfolio was the best performer in P&I's select universe, returning 12.1%, and outperforming its internal benchmark by 450 basis points for the year ended Sept. 30.

Other top performers in P&I's universe for the period:

the $2.5 billion hedge fund portfolio of the $29.5 billion South Carolina Retirement System Investment Commission, which exceeded its benchmark by 430 basis points with a 10.8% return; and

the $5.6 billion hedge fund portfolio of the New Jersey Division of Investment, which returned 10.5%, 270 basis points over its benchmark, on behalf of the $78.5 billion New Jersey Retirement System.

Aggregate hedge fund assets of the 16 public funds totaled $59.4 billion as of Sept. 30. The 16 funds had $951.3 billion in total assets.

Public plans' hedge fund returns

| Fund | Return | Benchmark | Over/ underperformance vs. benchmark (pct. pts.) |

Total hedge fund assets | Hedge fund assets as % of total assets |

|---|---|---|---|---|---|

| Missouri Public Schools

|

12.1% | 7.6% | 4.5 | $5.1 | 13.7% |

| South Carolina Retirement

|

10.8% | 6.5% | 4.3 | $2.5 | 8.6% |

| New Jersey Division of Investment | 10.5% | 7.8% | 2.7 | $5.6 | 7.1% |

| Pennsylvania State Employees

|

9.5% | 10.0% | -0.5 | $1.7 | 6.3% |

| Texas Teachers1 | 9.4% | 6.2% | 3.2 | $6.6 | 5.1% |

| Michigan Retirement System2 | 9.2% | 6.5% | 2.7 | $3.1 | 5.2% |

| New Mexico Public Employees | 9.2% | 6.1% | 3.1 | $1.1 | 7.7% |

| Texas County & District | 9.1% | 6.2% | 2.9 | $6.1 | 25.0% |

| Florida State Board3 | 9.0% | 9.4% | -0.4 | $2.8 | 1.9% |

| Massachusetts PRIM | 8.7% | 6.1% | 2.6 | $5.7 | 9.5% |

| Missouri State Employees | 8.5% | 6.5% | 2.0 | $2.0 | 22.1% |

| Texas Teachers4 | 7.6% | 5.6% | 2.0 | $5.2 | 4.0% |

| Illinois Teachers | 7.3% | 4.1% | 3.2 | $2.7 | 6.1% |

| Texas Employees5 | 6.9% | 4.1% | 2.8 | $1.5 | 5.9% |

| Pennsylvania Public Schools | 6.6% | 3.7% | 2.9 | $5.4 | 10.5% |

| Wisconsin Investment Board6 | 2.5% | 0.9% | 1.6 | $2.3 | 2.4% |

| MEAN RETURN | 8.6% | 6.1% | 2.5 | 8.8% | |

| MEDIAN RETURN | 9.1% | 6.2% | 2.8 |

Notes:

- Texas TRS directional portfolio;

- Hedge fund return is for the $43.6 billion Michigan Public School Retirement System; hedge fund assets and allocation are for all five MRS funds;

- Data are for Florida State Retirement System;

- Texas TRS stable value/non-directional portfolio;

- Returns are for Texas ERS' $1.3 absolute return portfolio; 6 Data are for Wisconsin State Retirement System Core Fund.

Source: Pension plan officials and plan documents

"New evolutionary stage"

"What's clear is that some larger public pension funds have entered a new evolutionary stage of hedge fund investment when they repurpose their portfolios to meet specific needs" of the overall pension fund, said Stephen L. Nesbitt, CEO of specialist alternative investment consultant Cliffwater LLC, Marina Del Rey, California.

The Missouri school fund, for example, uses 50% of the Barclays Capital Credit Intermediate index, 25% of the MSCI ACWI ex-U.S. (net) and 25% of the Russell 3000 index.

The blended benchmark better reflects the diversity of hedge fund strategies used in managing the 13.7% hedge fund allocation, which is managed a little differently from other pension funds, Mr. Tuck said.

In addition to strategies more typical of hedge fund portfolios - long/short equity, relative value, event-driven and global macro - Mr. Tuck and his team also invest in low-volatility equity, risk-parity, distressed credit and long exposure to real asset strategies through master limited partnerships.

A big advantage for the Missouri school fund program has been stability of investment staff and the board of trustees. The board gives Mr. Tuck's team discretion to move money among different strategies and managers.

"Good governance leads to good investment returns, and good investment returns give the board more confidence in the investment department's ability. It's a virtuous circle," said Mr. Tuck.

The Missouri school fund is among a group of public pension funds that also invest in hedge funds through a portable alpha strategy within domestic equity portfolios, but don't include those assets within their formal hedge fund program.

Another member of that group is the $14.3 billion Public Employees Retirement Association of New Mexico, Santa Fe, which has a $1.1 billion dedicated hedge fund portfolio and an additional $460 million in hedge fund assets managed in a portable alpha strategy within the domestic equity portfolio, said Jonathan Grabel, CIO.

New Mexico PERA's dedicated portfolio returned 9.2% for the year ended Sept. 30, exceeding the 6.1% return of its benchmark, the HFRI Fund of Funds Composite index, by 310 basis points.

Trustees approved investment guideline changes that permit staff to group hedge funds with similar strategies, Mr. Grabel said. While his staff has not started shifting assets from the dedicated portfolio yet, the fund has issued an RFP for a portable alpha manager, which could involve hedge funds.

The long-predicted move away from dedicated hedge fund allocations was evident during P&I's efforts to collect hedge fund portfolio returns.

Although returns of the best- and worst-performing institutional hedge fund portfolios were separated by 960 basis points, the broad range is purposeful, given that a number of the portfolios P&I analyzed are intended to be non-directional to avoid equity market beta.

The lowest return in P&I's ranking was the 2.5% one-year return of the $88.8 billion Wisconsin Retirement System. But the hedge fund portfolio topped its benchmark by 160 basis points and met the expectations of officials at the State of Wisconsin Investment Board, Madison, which manages the retirement system, said Vicki Hearing, a SWIB spokeswoman, in an e-mail.

"We are seeking a modest return profile and low to little correlation over time with markets, in particularly the stock market. SWIB has successfully implemented a hedge fund program that is part of its overall investment plan to use new investment strategies to help stabilize WRS Core Fund returns," Ms. Hearing said.

The Wisconsin hedge fund portfolio is benchmarked to the Dow Jones Credit Suisse Hedge Fund index, adjusted to reflect zero beta returns, Ms. Hearing said.

"Some pension funds are looking for hedge fund strategies that will provide them with pure alpha because they don't want to pay hedge fund fees for beta returns," Cliffwater's Mr. Nesbitt said.

"These pure alpha portfolios may appear to produce low returns, but they are high-quality returns," he added.

This article originally appeared in the December 22, 2014 print issue as, "Big public funds' portfolios outperform their indexes".

- Contact Christine Williamson at [email protected] | @Williamson_PI

Big Public Pension Funds' Hedge Fund Portfolios Outperform Their Indexes

Bucking persistent criticism of hedge fund returns coming from many quarters this year, chief investment officers of big state pension funds were able to report strong returns for their hedge fund portfolios.

Sources say public pension plan hedge fund portfolios by design did not keep pace with the returns of the S&P 500 and MSCI All-Country World indexes, which returned 19.7% and 12%, respectively, for the year ended Sept. 30.

That compares to the median one-year return of 9.1% of the 16 hedge fund portfolios in Pensions & Investments' universe as of Sept. 30.

The median of the big public funds topped the 6.4% return of the industry's most commonly used index - the HFRI (Hedge) Fund Weighted Composite, as well as MSCI InvestorForce's Trust Funds' median hedge fund returns for public and corporate defined benefit plans (7.1% and 7%, respectively) and endowments and foundations (6.7%).

"The broad universe of hedge funds tends to be long higher volatility and short lower volatility. We find that a broader mix of strategies is very helpful in smoothing out returns over time," said John Tuck, director of private equity and alternatives for the $37.5 billion Public School and Education Employees Retirement Systems of Missouri, Jefferson City.

That pension fund's $5.1 billion hedge fund portfolio was the best performer in P&I's select universe, returning 12.1%, and outperforming its internal benchmark by 450 basis points for the year ended Sept. 30.

Other top performers in P&I's universe for the period:

the $2.5 billion hedge fund portfolio of the $29.5 billion South Carolina Retirement System Investment Commission, which exceeded its benchmark by 430 basis points with a 10.8% return; and

the $5.6 billion hedge fund portfolio of the New Jersey Division of Investment, which returned 10.5%, 270 basis points over its benchmark, on behalf of the $78.5 billion New Jersey Retirement System.

Aggregate hedge fund assets of the 16 public funds totaled $59.4 billion as of Sept. 30. The 16 funds had $951.3 billion in total assets.

Public plans' hedge fund returns

| Fund | Return | Benchmark | Over/ underperformance vs. benchmark (pct. pts.) |

Total hedge fund assets | Hedge fund assets as % of total assets |

|---|---|---|---|---|---|

| Missouri Public Schools

|

12.1% | 7.6% | 4.5 | $5.1 | 13.7% |

| South Carolina Retirement

|

10.8% | 6.5% | 4.3 | $2.5 | 8.6% |

| New Jersey Division of Investment | 10.5% | 7.8% | 2.7 | $5.6 | 7.1% |

| Pennsylvania State Employees

|

9.5% | 10.0% | -0.5 | $1.7 | 6.3% |

| Texas Teachers1 | 9.4% | 6.2% | 3.2 | $6.6 | 5.1% |

| Michigan Retirement System2 | 9.2% | 6.5% | 2.7 | $3.1 | 5.2% |

| New Mexico Public Employees | 9.2% | 6.1% | 3.1 | $1.1 | 7.7% |

| Texas County & District | 9.1% | 6.2% | 2.9 | $6.1 | 25.0% |

| Florida State Board3 | 9.0% | 9.4% | -0.4 | $2.8 | 1.9% |

| Massachusetts PRIM | 8.7% | 6.1% | 2.6 | $5.7 | 9.5% |

| Missouri State Employees | 8.5% | 6.5% | 2.0 | $2.0 | 22.1% |

| Texas Teachers4 | 7.6% | 5.6% | 2.0 | $5.2 | 4.0% |

| Illinois Teachers | 7.3% | 4.1% | 3.2 | $2.7 | 6.1% |

| Texas Employees5 | 6.9% | 4.1% | 2.8 | $1.5 | 5.9% |

| Pennsylvania Public Schools | 6.6% | 3.7% | 2.9 | $5.4 | 10.5% |

| Wisconsin Investment Board6 | 2.5% | 0.9% | 1.6 | $2.3 | 2.4% |

| MEAN RETURN | 8.6% | 6.1% | 2.5 | 8.8% | |

| MEDIAN RETURN | 9.1% | 6.2% | 2.8 |

Notes:

- Texas TRS directional portfolio;

- Hedge fund return is for the $43.6 billion Michigan Public School Retirement System; hedge fund assets and allocation are for all five MRS funds;

- Data are for Florida State Retirement System;

- Texas TRS stable value/non-directional portfolio;

- Returns are for Texas ERS' $1.3 absolute return portfolio; 6 Data are for Wisconsin State Retirement System Core Fund.

Source: Pension plan officials and plan documents

"New evolutionary stage"

"What's clear is that some larger public pension funds have entered a new evolutionary stage of hedge fund investment when they repurpose their portfolios to meet specific needs" of the overall pension fund, said Stephen L. Nesbitt, CEO of specialist alternative investment consultant Cliffwater LLC, Marina Del Rey, California.

The Missouri school fund, for example, uses 50% of the Barclays Capital Credit Intermediate index, 25% of the MSCI ACWI ex-U.S. (net) and 25% of the Russell 3000 index.

The blended benchmark better reflects the diversity of hedge fund strategies used in managing the 13.7% hedge fund allocation, which is managed a little differently from other pension funds, Mr. Tuck said.

In addition to strategies more typical of hedge fund portfolios - long/short equity, relative value, event-driven and global macro - Mr. Tuck and his team also invest in low-volatility equity, risk-parity, distressed credit and long exposure to real asset strategies through master limited partnerships.

A big advantage for the Missouri school fund program has been stability of investment staff and the board of trustees. The board gives Mr. Tuck's team discretion to move money among different strategies and managers.

"Good governance leads to good investment returns, and good investment returns give the board more confidence in the investment department's ability. It's a virtuous circle," said Mr. Tuck.

The Missouri school fund is among a group of public pension funds that also invest in hedge funds through a portable alpha strategy within domestic equity portfolios, but don't include those assets within their formal hedge fund program.

Another member of that group is the $14.3 billion Public Employees Retirement Association of New Mexico, Santa Fe, which has a $1.1 billion dedicated hedge fund portfolio and an additional $460 million in hedge fund assets managed in a portable alpha strategy within the domestic equity portfolio, said Jonathan Grabel, CIO.

New Mexico PERA's dedicated portfolio returned 9.2% for the year ended Sept. 30, exceeding the 6.1% return of its benchmark, the HFRI Fund of Funds Composite index, by 310 basis points.

Trustees approved investment guideline changes that permit staff to group hedge funds with similar strategies, Mr. Grabel said. While his staff has not started shifting assets from the dedicated portfolio yet, the fund has issued an RFP for a portable alpha manager, which could involve hedge funds.

The long-predicted move away from dedicated hedge fund allocations was evident during P&I's efforts to collect hedge fund portfolio returns.

Although returns of the best- and worst-performing institutional hedge fund portfolios were separated by 960 basis points, the broad range is purposeful, given that a number of the portfolios P&I analyzed are intended to be non-directional to avoid equity market beta.

The lowest return in P&I's ranking was the 2.5% one-year return of the $88.8 billion Wisconsin Retirement System. But the hedge fund portfolio topped its benchmark by 160 basis points and met the expectations of officials at the State of Wisconsin Investment Board, Madison, which manages the retirement system, said Vicki Hearing, a SWIB spokeswoman, in an e-mail.

"We are seeking a modest return profile and low to little correlation over time with markets, in particularly the stock market. SWIB has successfully implemented a hedge fund program that is part of its overall investment plan to use new investment strategies to help stabilize WRS Core Fund returns," Ms. Hearing said.

The Wisconsin hedge fund portfolio is benchmarked to the Dow Jones Credit Suisse Hedge Fund index, adjusted to reflect zero beta returns, Ms. Hearing said.

"Some pension funds are looking for hedge fund strategies that will provide them with pure alpha because they don't want to pay hedge fund fees for beta returns," Cliffwater's Mr. Nesbitt said.

"These pure alpha portfolios may appear to produce low returns, but they are high-quality returns," he added.

This article originally appeared in the December 22, 2014 print issue as, "Big public funds' portfolios outperform their indexes".

- Contact Christine Williamson at [email protected] | @Williamson_PI

Tune in to stay informed about your retirement system, gain valuable insights, and hear from experts on how to make the most of your benefits. Join us for engaging discussions and essential updates designed with your needs in mind.

Life Events

When life brings changes your way, it can also impact your PSRS/PEERS membership. Click below for more information.

A New Member

Welcome! Your membership gives you distinct advantages when working toward a financially secure retirement. Get off to the right start and register for access to Web Member Services today.

Newly Married

If you are recently married, it can impact your beneficiary designations.

A New Parent

Birth or adoption of a child requires you to update your beneficiary designations.

Recently Divorced

If you named your spouse as a beneficiary, divorce means you may need to update your beneficiary designations. Some divorced retirees may also have options for benefit increases, or "pop-ups."

Moving

Keep your contact information up-to-date so we can communicate with you about your membership and ensure benefits are paid according to your wishes.

Ready to Retire

Apply for service retirement online using Web Member Services, or using paper forms found on this website.

Leaving Your Job

You have options when temporarily or permanently leaving covered employment.

A Working Retiree

It is important to understand post-retirement work limits and how they may impact your benefit payments.

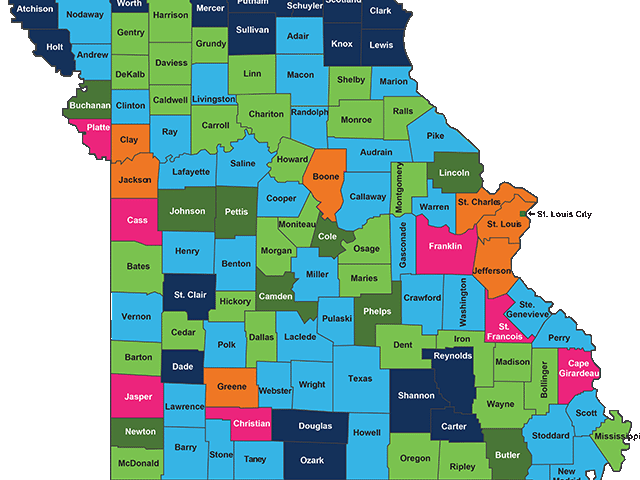

Benefits by County

As of June 30, 2025, approximately 113,000 individuals received benefits from PSRS/PEERS. Total annual benefits paid was nearly $4.0 billion. Of this amount, over $3.5 billion, or 88%, was distributed among Missouri's 114 counties, positively impacting the state's economy.

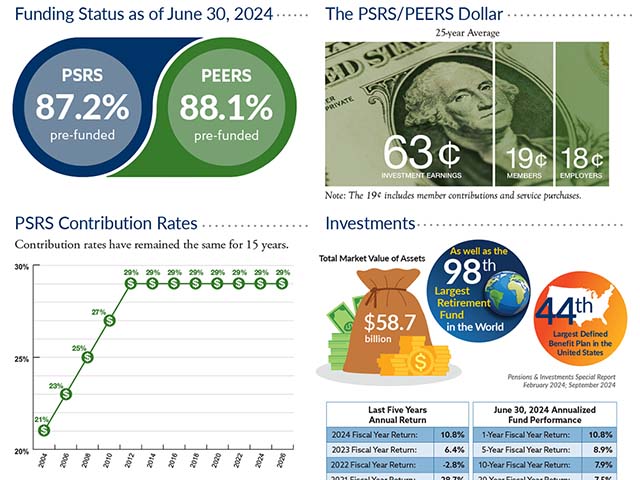

PSRS/PEERS Quick Facts

A summary of PSRS/PEERS statistics as of June 30, 2024.

PSRS/PEERS Funding

PSRS/PEERS' funding comes from three sources, member contributions, employer contributions and investment earnings. Investment earnings are the primary source of funding for every dollar of PSRS/PEERS benefits paid.