Member Tools

These tools and more are available in Web Member Services, the PSRS/PEERS online, self-service membership information portal. Click the links below if you already have a Web Member Services account or register to activate your account.

Tools for Active Members

- View Member Statements

- Estimate Service Retirement Benefits

- Calculate a Purchase Cost

- File for Service Retirement Online

- Designate or Update Beneficiaries

Tools for Retirees and Beneficiaries

Retirement Education

We want to help you learn more about your benefits and retirement system. Our counselors are here to help you get all the information you need, and offer a variety of educational opportunities to best fit your busy life.

View PSRS Education Options » View PEERS Education Options »PSRS/PEERS News

Actuarial Funding Policy Amended. PSRS Funding Status Remains Healthy

At the June 14, 2016 Public School and Education Employee Retirement Systems of Missouri (PSRS/PEERS) Board of Trustees meeting, the Board voted unanimously to amend the current Actuarial Funding Policy in various areas. The changes to the policy are, in part, a result of the recent Actuarial Experience Study and Asset Liability Study conducted by the System. These studies are conducted regularly and changes are applied as necessary to keep the System financially healthy.

The various assumptions within the Funding Policy that are being amended include inflation rates, payroll growth, mortality rates, investment returns, individual salaries, cost-of-living adjustments (COLAs), retirement rates and refund rates.

The objective of the PSRS Funding Policy is to achieve a funded ratio of 100% over a fixed period, not to exceed 30 years. The principles of the policy are to:

- Maintain adequate assets in order to fund all benefits expected to be paid to members and their beneficiaries

- Maintain stability of contribution rates

- Maintain accountability and transparency

- Promote intergenerational equality

- Provide a reasonable margin for adverse experience to help offset risks

- Review the investment earning assumption in conjunction with the Asset Liability Study and in consideration of the Board's investment risk profile and tolerance

- Review demographic and economic assumptions in conjunction with actual experience

This allows PSRS to continue progress toward reducing the System's unfunded liabilities, while keeping member and employer contribution rates at or near current levels.

The Big Impact on Pension Liabilities: Improved Mortality Rates; Lower Investment Returns

There are two key areas of change facing not only PSRS, but all retirement plans: improved life expectancies (mortality rates) and lower expected investment returns. Changes in these two areas have a significant impact on the financial condition of the System.

- People are living longer. Mortality is improving, not just in Missouri, but also across the nation. As a result, actuaries are utilizing updated mortality tables, which reflect this trend. PSRS conducted an Actuarial Experience Study to compare our actuarial assumptions to the actual experience of PSRS. In other words, are members living as long as we assumed they would, or are they actually living longer? "Educators, and people in general, are living longer and we have to account for that when looking at the liabilities of the System," said Board Chairman, Aaron Zalis. "The study shows we will be paying our members longer than was previously assumed." Consequently, the revised mortality assumptions better reflect PSRS' actual experience, which results in an increase of over $2 billion in liabilities to PSRS.

- Interest rates and future investment returns are projected to be lower than historical returns. This is reflected in the current low interest rate environment. As a result of a recently conducted Asset Liability Study, the System's investment consultant and actuaries recommended the PSRS assumed rate of return for investments be lowered from 8% to 7.75%. "The 30-year return history for the System remains above 8%. But with the volatile market environment we have seen this year, and will likely see for the next several years, changing the assumed rate of return was a prudent decision," stated Chief Investment Officer, Craig Husting. While the change seems modest, the impact is an increase in PSRS liabilities in excess of $1 billion.

Available Options

Due to the increase in liabilities the changes have on the financial stability of the System, the Board thoroughly explored the three areas in which they can positively impact the financial condition of the System: investment earnings, contribution rates and benefits.

Investment Earnings

The Board reviewed the current investment asset allocation looking for ways to increase PSRS' expected investment return. Upon review, and with the recommendation of the investment consultant, the System made minor changes to the asset allocation to optimize the investment portfolio. These modest changes will not materially impact the long-term PSRS expected return.

Expected investment returns and risk are highly correlated. Thus, if an investor takes on additional risk, there is an expectation for higher returns. However, the Board believes that the proposed asset allocation provides a prudent level of risk. It was determined that PSRS should not make major changes to the asset allocation that would cause the System to take on significantly more risk in hopes of improving returns.

Contribution Rates

As fiduciaries, PSRS Trustees have the important responsibility to annually set contribution rates to adequately fund the System. Rates are recommended annually by the System's actuaries, and by law cannot increase more than 1% per year. PSRS active members currently pay 14.5% of their salaries, with employers also paying 14.5%. The overall contribution rate of 29% is in line with the national average of similar plans. However, PSRS is unique in that both members and employers pay equal contribution amounts. Because of this, the PSRS employee contribution rate is currently one of the highest in the country.

Benefits

PSRS benefits are established under Missouri law. Consequently, the Board has very little flexibility within the law to alter the current benefit structure without action of the General Assembly. One area in which the Board has limited discretion is setting annual benefit increases in the form of COLAs.

| Change in Consumer Price Index (CPI-U) | Minimum Adjustment | Maximum Adjustment |

|---|---|---|

| <0% | 0% | 0% |

| 0%-2% | 0% | 5% |

| 2%-5% | 2% | 5% |

| >5% | 5% | 5% |

The factors evaluated by the Board when setting the COLA include:

- Changes in the cost of living reflected by the Consumer Price Index for Urban Consumers (CPI-U) for the preceding fiscal year

- The recommendation of the PSRS actuary based on the CPI-U and the PSRS Funding Policy

PSRS retirees are eligible for COLAs the second January following their retirement date. Since 2011, the PSRS Funding Policy stated that a 2% COLA would be granted in the years when the change in the CPI-U for the previous fiscal year was between 0% and 5%.

Because of the recent low CPI-U, this policy resulted in retirees receiving more than the actual CPI-U over the previous five years. The fiscal-year-to-date 2016 CPI-U remains considerably under the 2%, which would continue this trend.

The Impact of COLAs is Significant

It is important to note that COLA payments have a material effect on the overall cost of the retirement plan. The actuary has projected that the estimated cost of a one year 2% COLA is a $420 million increase in PSRS' liabilities.

The amended Funding Policy states that in years when the CPI-U for the previous fiscal year is between 0% and 2%, no COLA will be given. Changing the way COLAs are granted results in the following:

- PSRS experiences an overall savings of $2.5 billion in liabilities, which is expected to keep current contribution rates steady.

- The pre-funded status remains above 80%, which is considered a healthy status.

- Actuarial assumptions provide that retirees will still receive an average COLA of 1.5% over their retired lives.

- Retirees have peace of mind that the annual benefit increase will be 2% if actual inflation is 2% or greater.

- Retirees retain upside protection if inflation is high. If the CPI-U is greater than 5%, a 5% COLA would be granted.

- Active and retired members continue to share a commitment to the future financial health of the System. This is because COLAs are applied to both current and future benefits.

"As Trustees, our responsibility is to keep the System financially healthy. Amending the current Funding Policy is necessary in keeping with that responsibility," Zalis stated. "The Board feels the COLA change will help keep contribution rates steady, while at the same time, still provide protection against inflation when needed for our retirees. However, the overall financial health of the System and future contribution rates will be heavily influenced by investment markets moving forward."

The Goals Remain the Same

Implementation of all of these policy changes allows PSRS to continue to fulfill the Funding Policy objective and principals, as well as the overall goals of the System that have been in place since 1946.

- To provide retirement security to Missouri's educators and education employees after a full career of service

- To help school districts attract and retain the best and brightest educators and employees for Missouri's school children

- To manage the System in a prudent and cost efficient manner

The challenges of increased life spans and low interest rates are being felt by pension plans all across the county. It is important to note that PSRS remains in healthy financial condition. But making changes now only helps the System continue to provide strong, stable and secure retirement benefits for both current and future members.

Note: Similar changes to the Funding Policy also apply to the Public Education Employee Retirement System of Missouri (PEERS). PEERS active members currently pay 6.86% of their salaries, with employers also paying 6.86%. The total current PEERS contribution rate is 13.72%.

PEERS retirees are eligible for a COLA the fourth January following their retirement date.Actuarial Funding Policy Amended. PSRS Funding Status Remains Healthy

At the June 14, 2016 Public School and Education Employee Retirement Systems of Missouri (PSRS/PEERS) Board of Trustees meeting, the Board voted unanimously to amend the current Actuarial Funding Policy in various areas. The changes to the policy are, in part, a result of the recent Actuarial Experience Study and Asset Liability Study conducted by the System. These studies are conducted regularly and changes are applied as necessary to keep the System financially healthy.

The various assumptions within the Funding Policy that are being amended include inflation rates, payroll growth, mortality rates, investment returns, individual salaries, cost-of-living adjustments (COLAs), retirement rates and refund rates.

The objective of the PSRS Funding Policy is to achieve a funded ratio of 100% over a fixed period, not to exceed 30 years. The principles of the policy are to:

- Maintain adequate assets in order to fund all benefits expected to be paid to members and their beneficiaries

- Maintain stability of contribution rates

- Maintain accountability and transparency

- Promote intergenerational equality

- Provide a reasonable margin for adverse experience to help offset risks

- Review the investment earning assumption in conjunction with the Asset Liability Study and in consideration of the Board's investment risk profile and tolerance

- Review demographic and economic assumptions in conjunction with actual experience

This allows PSRS to continue progress toward reducing the System's unfunded liabilities, while keeping member and employer contribution rates at or near current levels.

The Big Impact on Pension Liabilities: Improved Mortality Rates; Lower Investment Returns

There are two key areas of change facing not only PSRS, but all retirement plans: improved life expectancies (mortality rates) and lower expected investment returns. Changes in these two areas have a significant impact on the financial condition of the System.

- People are living longer. Mortality is improving, not just in Missouri, but also across the nation. As a result, actuaries are utilizing updated mortality tables, which reflect this trend. PSRS conducted an Actuarial Experience Study to compare our actuarial assumptions to the actual experience of PSRS. In other words, are members living as long as we assumed they would, or are they actually living longer? "Educators, and people in general, are living longer and we have to account for that when looking at the liabilities of the System," said Board Chairman, Aaron Zalis. "The study shows we will be paying our members longer than was previously assumed." Consequently, the revised mortality assumptions better reflect PSRS' actual experience, which results in an increase of over $2 billion in liabilities to PSRS.

- Interest rates and future investment returns are projected to be lower than historical returns. This is reflected in the current low interest rate environment. As a result of a recently conducted Asset Liability Study, the System's investment consultant and actuaries recommended the PSRS assumed rate of return for investments be lowered from 8% to 7.75%. "The 30-year return history for the System remains above 8%. But with the volatile market environment we have seen this year, and will likely see for the next several years, changing the assumed rate of return was a prudent decision," stated Chief Investment Officer, Craig Husting. While the change seems modest, the impact is an increase in PSRS liabilities in excess of $1 billion.

Available Options

Due to the increase in liabilities the changes have on the financial stability of the System, the Board thoroughly explored the three areas in which they can positively impact the financial condition of the System: investment earnings, contribution rates and benefits.

Investment Earnings

The Board reviewed the current investment asset allocation looking for ways to increase PSRS' expected investment return. Upon review, and with the recommendation of the investment consultant, the System made minor changes to the asset allocation to optimize the investment portfolio. These modest changes will not materially impact the long-term PSRS expected return.

Expected investment returns and risk are highly correlated. Thus, if an investor takes on additional risk, there is an expectation for higher returns. However, the Board believes that the proposed asset allocation provides a prudent level of risk. It was determined that PSRS should not make major changes to the asset allocation that would cause the System to take on significantly more risk in hopes of improving returns.

Contribution Rates

As fiduciaries, PSRS Trustees have the important responsibility to annually set contribution rates to adequately fund the System. Rates are recommended annually by the System's actuaries, and by law cannot increase more than 1% per year. PSRS active members currently pay 14.5% of their salaries, with employers also paying 14.5%. The overall contribution rate of 29% is in line with the national average of similar plans. However, PSRS is unique in that both members and employers pay equal contribution amounts. Because of this, the PSRS employee contribution rate is currently one of the highest in the country.

Benefits

PSRS benefits are established under Missouri law. Consequently, the Board has very little flexibility within the law to alter the current benefit structure without action of the General Assembly. One area in which the Board has limited discretion is setting annual benefit increases in the form of COLAs.

| Change in Consumer Price Index (CPI-U) | Minimum Adjustment | Maximum Adjustment |

|---|---|---|

| <0% | 0% | 0% |

| 0%-2% | 0% | 5% |

| 2%-5% | 2% | 5% |

| >5% | 5% | 5% |

The factors evaluated by the Board when setting the COLA include:

- Changes in the cost of living reflected by the Consumer Price Index for Urban Consumers (CPI-U) for the preceding fiscal year

- The recommendation of the PSRS actuary based on the CPI-U and the PSRS Funding Policy

PSRS retirees are eligible for COLAs the second January following their retirement date. Since 2011, the PSRS Funding Policy stated that a 2% COLA would be granted in the years when the change in the CPI-U for the previous fiscal year was between 0% and 5%.

Because of the recent low CPI-U, this policy resulted in retirees receiving more than the actual CPI-U over the previous five years. The fiscal-year-to-date 2016 CPI-U remains considerably under the 2%, which would continue this trend.

The Impact of COLAs is Significant

It is important to note that COLA payments have a material effect on the overall cost of the retirement plan. The actuary has projected that the estimated cost of a one year 2% COLA is a $420 million increase in PSRS' liabilities.

The amended Funding Policy states that in years when the CPI-U for the previous fiscal year is between 0% and 2%, no COLA will be given. Changing the way COLAs are granted results in the following:

- PSRS experiences an overall savings of $2.5 billion in liabilities, which is expected to keep current contribution rates steady.

- The pre-funded status remains above 80%, which is considered a healthy status.

- Actuarial assumptions provide that retirees will still receive an average COLA of 1.5% over their retired lives.

- Retirees have peace of mind that the annual benefit increase will be 2% if actual inflation is 2% or greater.

- Retirees retain upside protection if inflation is high. If the CPI-U is greater than 5%, a 5% COLA would be granted.

- Active and retired members continue to share a commitment to the future financial health of the System. This is because COLAs are applied to both current and future benefits.

"As Trustees, our responsibility is to keep the System financially healthy. Amending the current Funding Policy is necessary in keeping with that responsibility," Zalis stated. "The Board feels the COLA change will help keep contribution rates steady, while at the same time, still provide protection against inflation when needed for our retirees. However, the overall financial health of the System and future contribution rates will be heavily influenced by investment markets moving forward."

The Goals Remain the Same

Implementation of all of these policy changes allows PSRS to continue to fulfill the Funding Policy objective and principals, as well as the overall goals of the System that have been in place since 1946.

- To provide retirement security to Missouri's educators and education employees after a full career of service

- To help school districts attract and retain the best and brightest educators and employees for Missouri's school children

- To manage the System in a prudent and cost efficient manner

The challenges of increased life spans and low interest rates are being felt by pension plans all across the county. It is important to note that PSRS remains in healthy financial condition. But making changes now only helps the System continue to provide strong, stable and secure retirement benefits for both current and future members.

Note: Similar changes to the Funding Policy also apply to the Public Education Employee Retirement System of Missouri (PEERS). PEERS active members currently pay 6.86% of their salaries, with employers also paying 6.86%. The total current PEERS contribution rate is 13.72%.

PEERS retirees are eligible for a COLA the fourth January following their retirement date.

Tune in to stay informed about your retirement system, gain valuable insights, and hear from experts on how to make the most of your benefits. Join us for engaging discussions and essential updates designed with your needs in mind.

Life Events

When life brings changes your way, it can also impact your PSRS/PEERS membership. Click below for more information.

A New Member

Welcome! Your membership gives you distinct advantages when working toward a financially secure retirement. Get off to the right start and register for access to Web Member Services today.

Newly Married

If you are recently married, it can impact your beneficiary designations.

A New Parent

Birth or adoption of a child requires you to update your beneficiary designations.

Recently Divorced

If you named your spouse as a beneficiary, divorce means you may need to update your beneficiary designations. Some divorced retirees may also have options for benefit increases, or "pop-ups."

Moving

Keep your contact information up-to-date so we can communicate with you about your membership and ensure benefits are paid according to your wishes.

Ready to Retire

Apply for service retirement online using Web Member Services, or using paper forms found on this website.

Leaving Your Job

You have options when temporarily or permanently leaving covered employment.

A Working Retiree

It is important to understand post-retirement work limits and how they may impact your benefit payments.

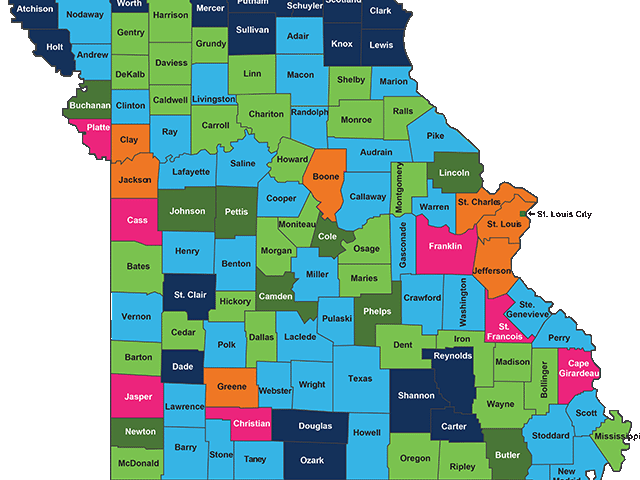

Benefits by County

As of June 30, 2025, approximately 113,000 individuals received benefits from PSRS/PEERS. Total annual benefits paid was nearly $4.0 billion. Of this amount, over $3.5 billion, or 88%, was distributed among Missouri's 114 counties, positively impacting the state's economy.

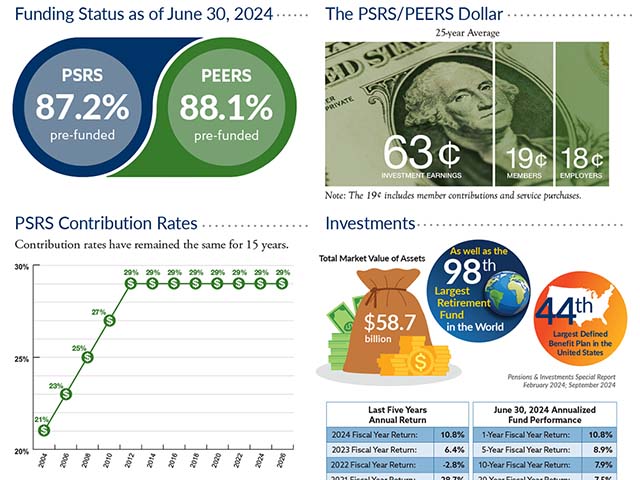

PSRS/PEERS Quick Facts

A summary of PSRS/PEERS statistics as of June 30, 2024.

PSRS/PEERS Funding

PSRS/PEERS' funding comes from three sources, member contributions, employer contributions and investment earnings. Investment earnings are the primary source of funding for every dollar of PSRS/PEERS benefits paid.